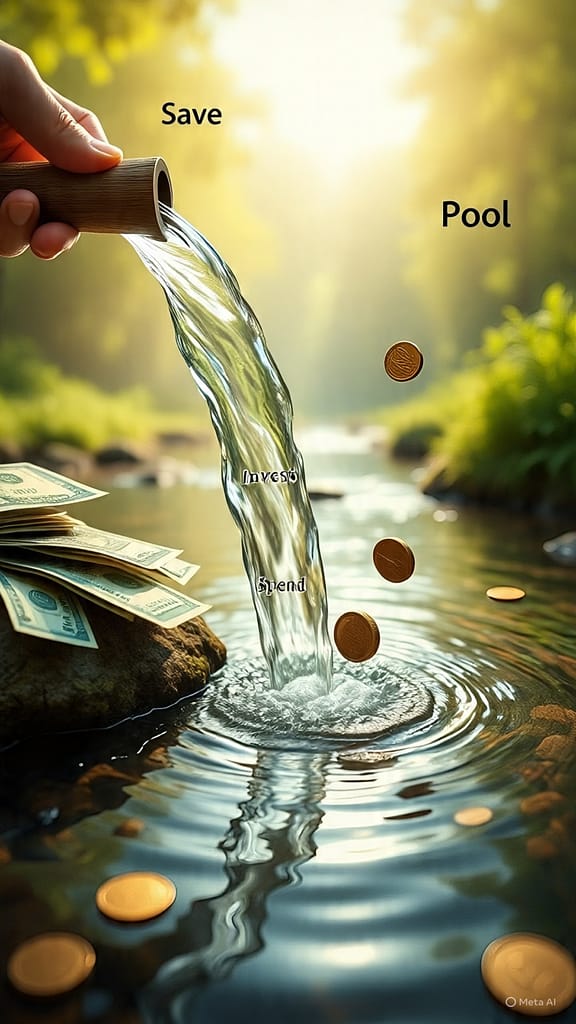

We call it “cash flow,” “liquidity,” and “drowning in debt” because money behaves exactly like water. It moves, pools, evaporates, leaks, floods, and sustains life—depending on how you engineer it.

Try to grip it in a closed fist and it escapes through the cracks. Ignore it and it goes stale. But channel it with intent, and it powers everything that matters to you. Here’s how the water analogy plays out, with examples you can act on this week.

Stagnant Money Turns Foul

Leave water in a sealed bottle for a year. It tastes flat and lifeless. Leave it in an open tank and it grows algae and breeds mosquitoes. Same H₂O, zero usefulness.

Cash sitting in a 0% account or a drawer does the same thing. Inflation is heat + time. It doesn’t steal your notes—it evaporates what they can buy.

Example: 1,800,000 PKR in 2010 could buy a brand new 1000cc hatchback. In 2026, that same 1,800,000 PKR buys a 12-year-old used one with high mileage. The paper didn’t disappear. Its buying power evaporated while it sat still.

Fix: Keep money moving. High-yield savings, T-bills, sukuk, index funds, REITs, rental income, or skills that raise your hourly rate. Moving water stays fresh. Moving money stays competitive.

No Channels = Mud. No Budget = Mystery.

Pour 8,000 liters onto bare ground. It spreads, turns to mud, and sinks into cracks. You can’t collect or reuse it. That’s not irrigation—it’s loss.

That’s a paycheck with no plan. Salary lands and instantly seeps into food delivery, flash sales, “small” upgrades, and weekend impulses. By the 10th you’re checking your app thinking, “Where did it go?”

Example: Sana earns 480,000 PKR/month. For years she saved nothing despite strong income. She installed “plumbing”: 96,000 PKR auto-invests on the 1st, 72,000 PKR to emergency fund, 240,000 PKR to bills/rent, 72,000 PKR guilt-free spending. Same income, different outcome. The pipes gave every rupee a job before it could turn to mud.

A budget isn’t a cage. It’s irrigation. It creates pressure and direction so money feeds the right fields.

Dams Need Spillways. Savings Need Circulation.

A dam that only stores water is a future disaster. One heavy monsoon and the wall cracks, flooding everything downstream.

Many people build a financial dam: “I’ll just save until I feel safe.” They hit 11M PKR and stop. No investments, no side income, no new skills. Then a layoff + medical emergency hits in one quarter. The reservoir empties in 15 months, and rebuilding takes years.

Example: Talha saved 10.5M PKR over 18 years. In 2024 he was jobless for 15 months while funding his daughter’s treatment. The dam drained. If he’d channeled 30% into dividend ETFs or steady freelance clients during the good years, he’d still have inflow. Storage alone isn’t strategy. Circulation is.

Rule: Reservoir + Channels + Spillway. Emergency fund + Investments + Income skills. Hold some, flow some.

Drips Drain Tanks. Small Spends Drain Wealth.

A tap dripping once per second wastes ∼30 liters a day. That’s 10,950 liters a year—your whole tank—through a hole you barely hear.

Money leaks are identical. The 1,600 PKR daily specialty coffee + muffin. The 8,000 PKR/month apps you forgot. The 3,000 PKR “free delivery” add-ons.

Example – Your Yearly Leak:

- Daily drinks/snacks: 1,600 x 2 x 24 = 76,800 PKR/month

- Forgotten subscriptions: 18,000 PKR/month

- Convenience + impulse fees: 16,000 PKR/month

- Total: 110,800 PKR/month = 1,329,600 PKR/year

That’s a small car paid in cash. That’s two years of maxing out investments. That’s a full emergency fund plus premium insurance for the family. All gone through pinholes you never patched.

Run a leak audit every 90 days. Cancel two subscriptions. Redirect that stream to “Grow” or “Guard.”

We Reroute Rivers. You Can Reroute Your Habits.

The most powerful fact about water: humans move it. We cut canals through deserts and built aqueducts across mountains. We turned barren land into farmland with planning and work.

Your spending is a riverbed carved by habit. Right now it might flow into credit card interest and lifestyle inflation. Pick up a shovel.

Example: Komal had 4.8M PKR in cards and personal loans. Her river poured into 39-46% interest. She dug a new trench: sold her financed SUV, bought a 1.6M PKR cash car, and pointed the freed 120,000 PKR/month at debt. 35 months later: debt zero. That same 120k now flows into her portfolio. Same water, new harvest.

You don’t always need more rain. You need better irrigation.

The 3-Channel System: Engineer Your Flow

Assign every rupee the moment it arrives:

- Live – 50-60%: Rent, food, transport, utilities, essentials. Runs today.

- Grow – 20-30%: ETFs, stocks, business, courses, tools, property. Builds tomorrow.

- Guard – 10-20%: Emergency fund, insurance, debt payoff. Prevents floods and droughts.

If 100% flows into “Live,” you’re farming in a floodplain. One bad season and you’re underwater.

Bottom line: Don’t worship money and don’t fear it. Treat it like water. Channel it. Don’t dam it forever. Patch the leaks, dig smart trenches, and keep it moving.

Water that’s channeled powers cities and feeds millions. Water that’s spilled just makes mud.

Your move this week: Find one leak. Plug it. Point that stream at “Grow” or “Guard.” Check back in 90 days and see what changed.